What Is a Credit Score?

A credit score is a number between 300–850 that depicts a consumer’s creditworthiness. The higher the score, the better a borrower looks to potential lenders. A credit score is based on credit history: number of open accounts, total levels of debt, and repayment history, and other factors. Lenders use credit scores to evaluate the probability that an individual will repay loans in a timely manner.

KEY TAKEAWAYS

- A credit score plays a key role in a lender’s decision to offer credit.

- The FICO scoring system is used by many financial institutions.

- Factors considered in credit scoring include repayment history, types of loans, length of credit history, and an individual’s total debt.

- One metric used in calculating a credit score is credit utilization or the percentage of available credit currently being used.

- It is not always advisable to close a credit account that is not being used since doing so can lower a person’s credit score.

The credit score model was created by the Fair Isaac Corporation, also known as FICO, and it is used by financial institutions.5 While other credit-scoring systems exist, the FICO score is by far the most commonly used. There are a number of ways to improve an individual’s score, including repaying loans on time and keeping debt low.

How Credit Scores Work

A credit score can significantly affect your financial life. It plays a key role in a lender’s decision to offer you credit. People with credit scores below 640, for example, are generally considered to be subprime borrowers. Lending institutions often charge interest on subprime mortgages at a rate higher than a conventional mortgage in order to compensate themselves for carrying more risk. They may also require a shorter repayment term or a co-signer for borrowers with a low credit score.

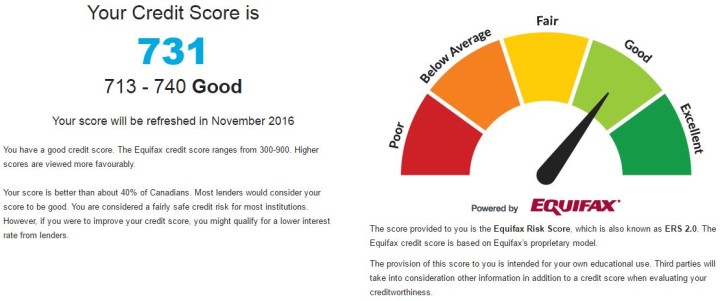

Conversely, a credit score of 700 or above is generally considered good and may result in a borrower receiving a lower interest rate, which results in their paying less money in interest over the life of the loan. Scores greater than 800 are considered excellent. While every creditor defines its own ranges for credit scores, the average FICO score range is often used:6

- Excellent: 800 to 850

- Very Good: 740 to 799

- Good: 670 to 739

- Fair: 580 to 669

- Poor: 300 to 579

Your credit score, a statistical analysis of your creditworthiness, directly affects how much or how little you might pay for any lines of credit you take out.

A person’s credit score may also determine the size of an initial deposit required to obtain a smartphone, cable service or utilities, or to rent an apartment. And lenders frequently review borrowers’ scores, especially when deciding whether to change an interest rate or credit limit on a credit card.

Credit Score Factors: How Your Score Is Calculated

There are three major credit reporting agencies in the United States (Experian, Equifax, and Transunion), which report, update, and store consumers’ credit histories. While there can be differences in the information collected by the three credit bureaus, there are five main factors evaluated when calculating a credit score:

- Payment history

- Total amount owed

- Length of credit history

- Types of credit

- New credit

How to Improve Your Credit Score

When information is updated on a borrower’s credit report, their credit score changes and can rise or fall based on new information. Here are some ways a consumer can improve their credit score:

- Pay your bills on time: Six months of on-time payments is required to see a noticeable difference in your score.

- Up your credit line: If you have credit card accounts, call and inquire about a credit increase. If your account is in good standing, you should be granted an increase in your credit limit. It is important not to spend this amount so that you maintain a lower credit utilization rate.

- Don’t close a credit card account: If you are not using a certain credit card, it is best to stop using it instead of closing the account. Depending on the age and credit limit of a card, it can hurt your credit score if you close the account. Say, for instance, that you have $1,000 in debt and a $5,000 credit limit split evenly between two cards. As the account is, your credit utilization rate is 20%, which is good. However, closing one of the cards would put your credit utilization rate at 40%, which will negatively affect your score.

- Work with one of the best credit repair companies: If you don’t have the time to improve your credit score, credit repair companies will negotiate with your creditors and the three credit agencies on your behalf, in exchange for a monthly fee.

{kind=link}