If you have a 650 credit score, you may be wondering what that means. Is 650 a good credit score, a bad score, or somewhere in between? What does having a 650 credit score mean for your wallet? Read on to find out all you need to know about having a 650 credit score.

650 credit score basics

While there are different models and algorithms for calculating your credit score, for the purposes of this article, we’re going to talk about your FICO Score. A FICO Score is a three-digit number, ranging from 300 to 850, and the higher your score, the better. A 650 FICO score is generally considered to be Fair.

If you have a 650 credit score, you may still be denied some loans and credit cards — and you may be forced to pay higher interest rates for the ones you are approved for. You need at least a 700 score to have Good credit — but 650 isn’t considered Poor either. Rest assured that a little bit of credit improvement can result in saving a lot of money.

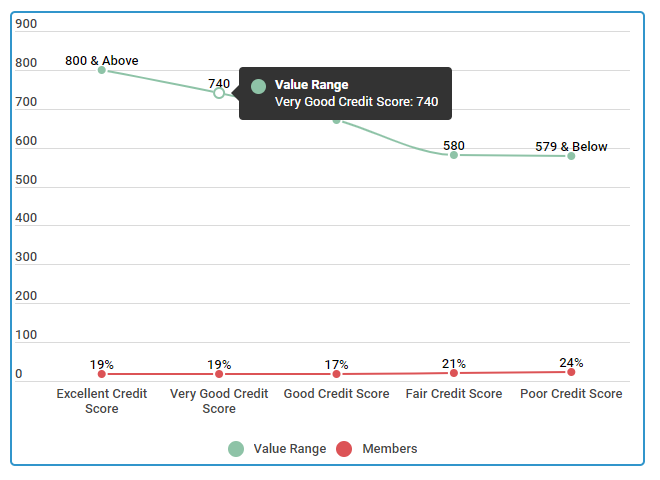

The chart below shows the various credit range scores. As you can see, if you have a 650, you fall into the Fair category, along with 21 percent of our credit sesame members.

Comparing Credit Score Ranges of Credit Sesame Members

Show 102550100 entriesSearch:

| Score Range | Value Range | Members |

|---|---|---|

| Excellent Credit Score | 800 & Above | 19% |

| Very Good Credit Score | 740 – 799 | 19% |

| Good Credit Score | 670 – 739 | 17% |

| Fair Credit Score | 580 – 669 | 21% |

| Poor Credit Score | 579 & Below | 24% |

Showing 1 to 5 of 5 entriesPreviousNextSource: Credit scores were calculated from 5,000 Credit Sesame members on 2/6/18.

Now you know you are not alone in having a 650 credit score, let’s find out more about your credit score and the steps you can take to help you increase it.

How to improve your 650 credit score

If your credit score isn’t where you want it to be, don’t fret — there are steps that you can take to help build and improve your credit:

- Make all of your payments on time — every time. This is the single biggest thing you can do to help improve your credit score. Consistently making your payments on time will lead to a steady increase in your credit score.

- Reduce your credit utilization. Your credit utilization is a ratio of the amount of debt you currently owe to the sum of your total credit limits. The lower this number, the better — so always aim to use less than 30 percent of your available credit at any given time.

- Limit the number of hard inquiries. While it doesn’t hurt your score to check your credit yourself (a soft inquiry), a hard inquiry, such as when applying for a new credit card, can ding your score slightly. Limit the number of credit applications to see a rise in your score.

These are just a few of the steps you can take to improve your credit, but there are many different steps and strategies to improve your credit score. However, the data below shows how some of our Credit Sesame members were able to improve their score over three months, six months, and 12-months using some of these strategies.

For example, by reducing their debts, members increased their 650 score by two percent in just three months, four percent in just six months, and nine percent in 12 months.