You know your credit score is important, but what exactly does that three-digit number mean when it comes to securing a car loan? In this post, we’ll explain what your credit score means and how it’s calculated.

How do credit scores work in Canada?

In Canada, credit scores range from 900 points (the highest score) down to 300 points. According to TransUnion, a score above 650 will likely qualify you for a standard loan, while a score under 650 will likely bring difficulty in receiving new credit.

What is a good credit score in Canada?

A credit score of 680 or above is generally considered good. 780 or above is considered to be excellent, while 900 is perfect. Most credit scores fall between 620 and 679. Higher scores indicate better credit decisions and can make lenders more confident that you will repay your future debts as agreed.

How to check your credit report in Canada

There are two national credit bureaus in Canada: Equifax Canada and TransUnion Canada. You can get a free copy of your credit report by mail in two to three weeks once you have provided your identification and some basic information. Be sure to check with both bureaus.

If you need a credit report sooner you can get one online from both bureaus for a fee of less than $20. Keep in mind that your number might differ slightly between companies because of their unique algorithms.

What your credit score means

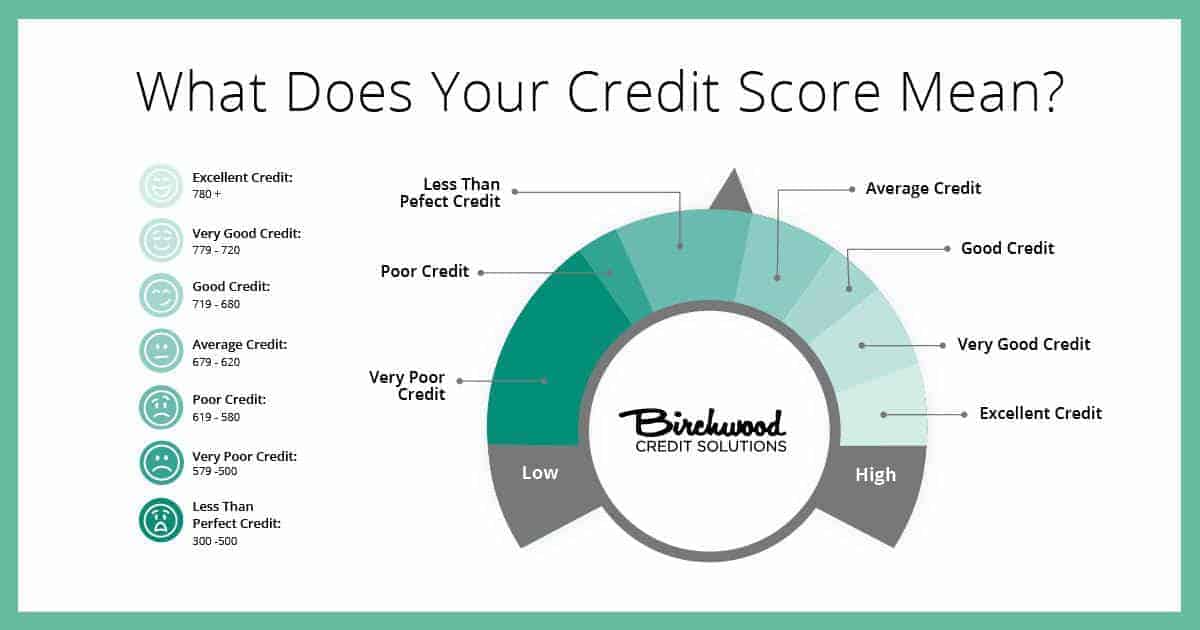

Now that you have your credit report, you need to decipher your score and figure out where you land on the creditworthiness scale. We’ll start at the top of the range and work our way down:

780+: Excellent credit. You can access the best interest rates on the market and will typically be approved for a loan.

779-720: Very good credit. Your credit is near perfect and you will enjoy very good interest rates.

719-680: Good credit. You will have little to no trouble getting approved for financing.

679-620: Average credit. The majority of borrowers fall in this range in Canada. You will have slightly higher interest rates than someone with a higher number.

619-580: Poor credit. If you land in this range, you’re what lenders deem “high risk.” You might have a hard time getting a loan and will have high interest rates.

579-500: Very poor credit. You will rarely be approved for financing,

300-500: Terrible credit. If you have a score of less than 500 you have bad credit and it will be very difficult to get approved for any kind of loan. You should work on improving your credit.

That range probably looks intimidating, especially if you fall on the low end of the scale. But, the good news is that it’s possible to improve your credit score with a little work and some good advice.

How is credit score calculated in Canada?

Your credit score is calculated through six main categories and is representative of how well you manage your credit responsibilities.

FACTORS AFFECTING CREDIT SCORE IN CANADA

There are six main factors that affect the calculation of your credit score. These are the areas that you should focus on if you’re interested in improving your credit score.

- Payment History: This reflects how frequently you pay your debts or bills on time and it is the biggest thing that affects your credit score. If you want to improve your number, your main priority should be paying your bills on time.

- Used Credit vs. Available Credit: This is the second largest contributor to your score and it refers to the amount you owe compared to your credit limit. It’s a good idea to avoid running your balance up to your limit, as that can harm your score.

- Credit History: Because good credit is built over time, how long you’ve had credit plays a role in your score. Lenders want to know that you can handle credit accounts over a period of time.

- Diversity: Lenders also want to know that your can handle a mix of different kinds of credit at once, such as credit cards, loans and mortgages. The more diverse your credit, the higher your score.

- Public Records: If you’ve claimed bankruptcy in the past or have had prior collection issues, these will be factored into your score.

- Inquiries: Your credit score takes a small and temporary hit each time a lender accesses your file; however, your score will drop if you apply for a bunch of new credit in a short period of time. This does not apply to pre-approvals or personal credit report requests.

How to improve your credit score

With so many different things affecting your credit score, tackling your credit situation might seem like a daunting task. The good news is that your low score doesn’t have to be looming over you forever because you have the power to improve your credit score.